A balance sheet shows your debts, assets and equity. It’s an important financial statement that lenders and investors will likely ask to see. Here’s how to create one and how to avoid common balance sheet mistakes.

Every small business owner needs to be familiar with three important documents: a profit and loss statement, a cash flow statement and a balance sheet. Getting money from lenders and investors may very well depend on them.

They all go hand-in-hand to give you a full picture of your business’ financial standing. A balance sheet is a snapshot of how much money your business has and how much it needs to pay. More specifically, it shows your assets, liabilities and equity.

Not sure what those mean? Here’s a breakdown:

Assets |

What it means: Cash or anything your business has that can be converted into cash. Current assets can be quickly converted into cash while non-current assets can take over a year to become cash. Examples: Cash, property, land, equipment |

Liabilities |

What it means: Money you owe for goods or services you’ve already received. Current liabilities are debts due within a year and long-term liabilities are debts due in over a year. Examples: Loans and interest, salaries, taxes, mortgage |

Equity

Also known as:shareholders' equity

|

What it means: The amount you would have if you paid off all your debt and all your assets were cashed out. Examples: Retained earnings, owner’s draw, current year earnings |

A balance sheet only shows your business’ standings at a specific point in time. It’s one of the most important tools you’ll need to show how your business is doing.

Why do I need a balance sheet?

One of the most important reasons you need a balance sheet is because investors and lenders will almost always ask to see it before giving you their business. They want to know if giving you money will be risky for them — which they can determine by looking at your debt.

Your balance sheet is just as important for you as it is for investors and lenders. It’s an objective way to see where your business is standing financially. It can also help you make big business decisions and answer key questions like these:

- Can I afford to take on more debt and buy a new office space?

- How much money do I owe?

- Can I afford to pay off my current debt?

To get a fuller picture of your business’ standings, analyze your balance sheet alongside your profit and loss statement and cash flow statement.

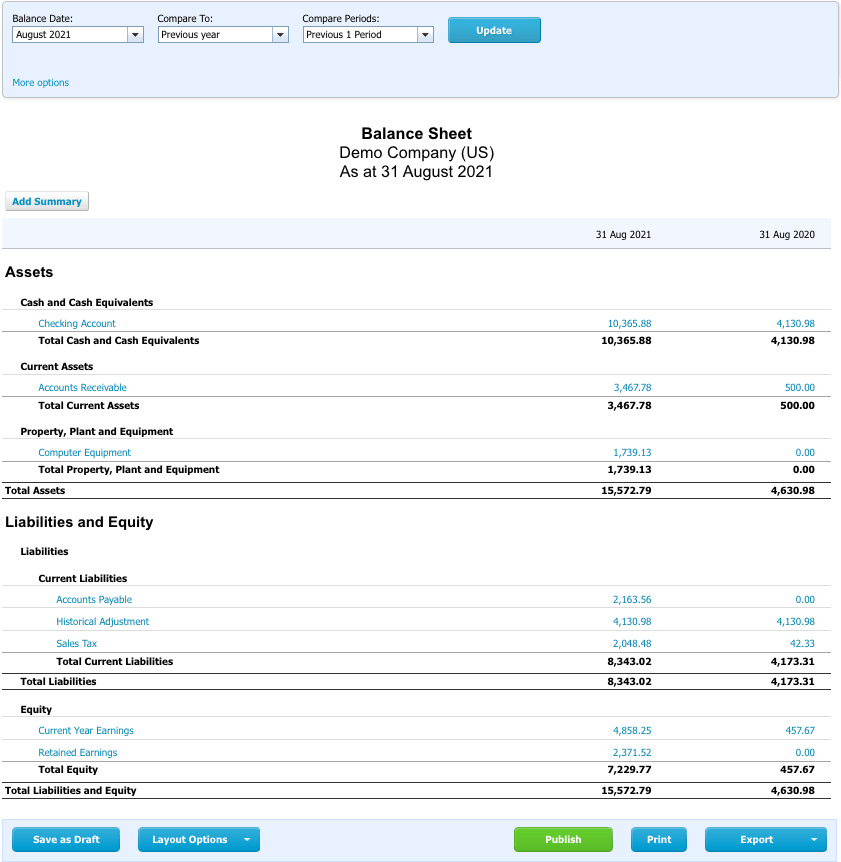

Balance sheet example

Many big corporations like Amazon and Apple are required to make their balance sheets public. However, theirs are much longer and more complicated than your small business balance sheet should be.

Below is a balance sheet pulled by Xero, the accounting software that we recommend most small business owners use. But if you use another software or just do it yourself, it should look very similar.

Balance sheets only capture a snapshot of your business at a specific point in time, and not over a period of time. The two dates in the right columns on this balance sheet are two “snapshots” taken a year apart.

This is a common practice for creating balance sheets, because it can show how your assets have grown from one month, quarter or year to the next.

How to create a balance sheet

Your first option for creating a balance sheet should always be pulling it from your accounting software. Since your software is connected to your bank accounts, it can give you the most accurate figures.

If you don’t have accounting software or a bookkeeper that can do your balance sheet for you, then follow these steps to create your balance sheet.

1. Choose which date you want your balance sheet to reflect

Your balance sheet doesn’t show a period of time, it only reflects your finances on a particular day. Many balance sheets include figures from two points of the year to see what direction the business is heading.

2. Calculate your assets

Assets are your money on hand and things your business owns that can be sold for cash value. As defined earlier, the two types of assets are current and non-current assets. They may also be called liquid or non-liquid assets.

Current assets are types of assets you could cash out relatively quickly. Non-current assets can take more than a year until you ever see the cash from it.

These are a few common examples you might list on your balance sheet:

- Cash

- Land

- Equipment

- Buildings

- Cars

3. Calculate liabilities

Liabilities are debts you owe. Like assets, there are two types: current and long-term liabilities.

Current liabilities are due in less than a year and long-term liabilities aren’t due for a year or more. Regardless of when they’re due, they need to go on your balance sheet.

These are some common examples of liabilities you would list on your balance sheet:

- Car loans

- Mortgages

- Salaries and wages

- Credit cards

- Taxes

4. Calculate equity

Equity is what you would have if you liquidated all your assets and paid off all your debt today.

Depending on the type of business you have, this may be called shareholder or stockholder equity. On a balance sheet, you’ll often see equity and liabilities lumped together. That’s because your equity and liabilities should equal your assets.

You should list these under the equity portion of a balance sheet:

- Retained earnings

- Owner’s capital

- Common stock

5. Make your sure your balance sheet balances

This step is the most important part of creating your balance sheet. Once you calculate your assets, liabilities and equity, you need to confirm if your balance sheet, well, balances. That means this equation needs to hold true on your balance sheet.

| Assets = Liabilities + Equity |

If it doesn’t add up, then a few things may have gone wrong. You might have calculated your amounts incorrectly, or just made a typo while transferring your numbers. Either way, you need to fix it by going through your calculations again or talking to your bookkeeper.

Common balance sheet mistakes

Although balance sheets are simple reports, you can mess them up pretty easily. These are the top two common mistakes small business owners often make when creating their first balance sheets — and how to avoid them.

Creating it manually

Avoid creating your balance sheet from scratch or even from a template, if you can. Inputting every amount manually creates a lot more room for error.

You can end up with an unbalanced balance sheet, which is one where your assets don’t equal your liabilities plus equity, if you slip up and get even one digit wrong. That’s a problem because investors and lenders can see the slip-up and choose not to do business with you.

The fix: The most efficient way to create your balance sheet is to pull it from the accounting software you use. The earlier example is from Xero, but any other software most likely has the option to pull your balance sheet as well.

Classifying accounts wrong

It’s important to understand the differences between assets, liabilities and equity. If you mislabel accounts, that could mislead you or investors.

For example, imagine you received a $50,000 loan. You now have $50,000 more than you previously had, but that’s not technically revenue. You have to pay it back, so it’s really a liability. By labeling that as revenue, that leads you or investors to believe you generated $50,000 more in revenue — but it's really income from a loan, which is a liability.

Whether it’s a loan, car, building or something else, it’s important to understand how a purchase or loan can affect both your assets and your liabilities. If you don’t, your balance sheet may be unbalanced, which creates a problem for you and investors.

The fix: Create your first balance sheets with the help of a bookkeeper or accountant. They can help you differentiate between assets, liabilities and equity so you can create an accurate balance sheet.

The bottom line

Your balance sheet is the scorecard of your business. It’s a crucial financial report that lets both you and investors know how well your business is performing.

The best way to create a balance sheet is by pulling it from your accounting software. That creates the most accurate balance sheet so you can make important decisions for your business based on the right information.

If you’re a new business owner creating a balance sheet for the first time, you’ll likely benefit from reviewing it with a bookkeeper. They can teach you how to read your balance sheet and give you personalized recommendations for how to grow your business.

Click the button below to schedule a free call with a DiMercurio Advisors team member today and understand your balance sheet.