Tossing a hurricane into the mix of running a business is stressful. However, understanding how the hurricane impacts your taxes doesn’t have to be. Being a native Floridian that has experienced many hurricanes (starting with the dreaded Hurricane Andrew over 30 years ago), I’ve seen firsthand how even mentioning a hurricane or storm can have an impact on your business.

I’ve put together this article to help you understand what your options are in plain language so you can make decisions quickly about your business.

Summary

- If your business was impacted by a hurricane, you’ll probably have some lost revenue, repair costs and possibly insurance proceeds.

- Lost revenue usually can’t be deducted because you didn’t receive it.

- Money paid for repairs and to protect your business are deductible.

- If your real estate declined in value or suffered damage due to the hurricane, you can take a business casualty loss.

- Insurance proceeds can be tricky, usually they’re included in income.

- Bookkeeping for hurricane expenses can be tricky, we’ve given you some helpful tips on how to do this.

- The IRS will push back deadlines when a federal disaster area is declared.

- Even if you don’t live in the disaster area, you might be able to follow the disaster rules.

Can I deduct lost revenue?

Probably not.

Why? Because you can’t deduct something that didn’t happen. While you did lose potential future value, the IRS only works in the present, on what has happened, not what could have happened.

However, if you have business interruption insurance, you could have some money coming to you for that lost potential revenue.

Be aware that any payments you receive from your business interruption insurance will be considered taxable income. This is because it’s a payment to replace the revenue you would have received, and revenue is taxable.

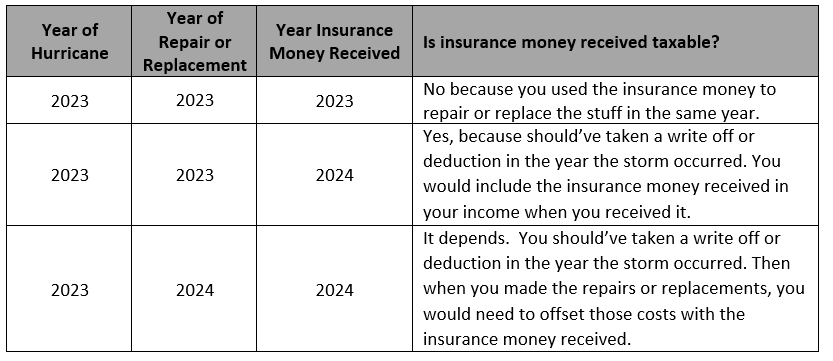

Are insurance payments I receive taxable?

It really depends on three dates:

- The year of the hurricane

- The year you repaired and/or replaced what was destroyed or declined in value

- The year you received the insurance proceeds

What happens when you receive more insurance money than you actually spent? You would pick up the difference as additional income. This could play through as you taking a deduction in one year and then picking up the income in another.

What if my stuff was damaged?

The rules are fairly simple here. When something that you could be using in your business is damaged or destroyed and you have to “toss it out” you get a tax deduction for tossing it out. However, you can only write off up to the adjusted basis in the thing that you tossed out.

We’re going to break this down into three separate categories and walk through each of them with you:

- Inventory destroyed: This is either the raw goods you use to make your final products or the final products that you have for sale. These are likely to be destroyed when a hurricane causes damage to your production facility, warehouse or the like.

- Equipment destroyed: Think of office equipment, computers, printers, machinery, all the non-real estate stuff that you own. When a roof is destroyed or when a window breaks in your office building it is likely the equipment inside can be damaged or destroyed.

- Real estate partially or completely destroyed: This is any physical buildings or real estate that you own, including office buildings, homes for rent, multi-family apartment units, vacation rentals and so on.

Inventory destroyed

When inventory is destroyed, you can write it off as long as its tossed. If you keep it, the IRS will assume it’s still good, and thus it can’t be written off. Our recommendation here is to toss it or have a written plan to toss it out as soon as possible.

If insurance money is received to replace the inventory, the insurance proceeds would offset the write off. For example, let’s say you have $35,000 of inventory that was destroyed and you receive a check for $15,000 to replace the inventory from your insurance company. What it looks like on your books depends on when you received the insurance money:

- If received in the same year as the hurricane, then you would have a net inventory loss of $20,000 (the $35,000 worth of inventory less the $15,000 insurance money)

- If you received it in a later year, you would have a $35,000 inventory loss in the year of the hurricane and a $15,000 inventory insurance proceeds income in the year you received the insurance money.

You can also write off any costs associated with the loss of the inventory in the year it was incurred. This could include extra labor, renting vehicles and trailers and so on.

Equipment destroyed

If the equipment used to run your business (computers, tables, chairs, machinery, etc.) is destroyed during the storm, you can write it off up to the amount of your adjusted basis.

This can be tricky because if you took the 100% bonus or Section 179 depreciation expense in a prior year, then your adjusted basis in the property would be $0. Meaning, there’s no tax deduction to receive. However if you haven’t fully depreciated the equipment, you will be able to take tax a deduction for the remaining adjusted basis left.

If you receive insurance money to purchase replacement equipment, you would:

- Write off the remaining adjusted basis of the asset that was destroyed.

- Record the insurance money received as insurance income. This would be taxable in the year you receive it.

- Record the purchase of the replacement equipment as a new asset on your books. You would also get to take bonus or Section 179 depreciation expense for this purchase in the year you put the asset in service.

Real estate partially or completely destroyed

When we say real estate, we mean property you are using in your business. That could be an office building, apartment complex, vacation rental, and so on. It rarely ever means raw land, unless you are renting that land under a land lease or similar deal. If real estate that is used in your business is destroyed, then a business casualty loss deduction can be taken and it’s reported on Form 4684 as part of your income tax return.

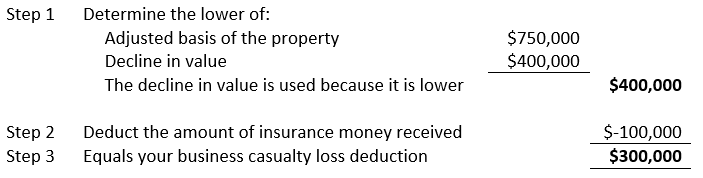

Your business casualty loss deduction amount is the lesser of:

- Your adjusted basis in the property, or

- The difference between the value of the property immediately before the hurricane and the value of the property immediately after the hurricane

The IRS has specific rules related to the valuation of the property. The value shown on your property tax bill either can’t be used. The IRS typically will want an actual appraisal or valuation report by an independent third party. In certain circumstances, the cost of the repairs can be used to determine the decrease in property value.

Let’s run through an example. You paid $1,000,000 for a building. You have taken $250,000 of depreciation on the building, so the adjusted basis of that building is $750,000. Immediately prior to the storm that property was worth $2,000,000. Immediately after the storm, the property was worth $1,600,000, a $400,000 decline in value. You also received $100,000 in insurance payments in the same year. How much is the business casualty loss deduction?

If repairs and/or improvements must be made to the property, the adjusted basis in the property must be increased by those amounts. The key reason here is to prevent double dipping: If you take a deduction for the business casualty loss, then you can’t also take a deduction for improving the property. Because of this, you should determine what would make more sense: deducting the repair costs or taking the business casualty loss.

What year can I take the deduction?

This is cool! You have two options here! Take the deduction in the year of the hurricane or, if FEMA declared a federal disaster area and you experienced a business casualty loss, then you could amend your prior year income tax return.

Here’s what you need to know.

When does the election have to be made?

This can get a little tricky, so here’s a quick visual explanation:

The official rule is “the due date for making the election is six months after the due date for filing your income tax return for the year the hurricane occurred (without extensions)”. Most businesses file their tax returns by March 15th, thus you can take a loss from a hurricane in 2023 and amend your 2022 tax return to claim the casualty loss deduction as late as September 15, 2024 (which would be six months after the 2023 tax return was due).

Are there any cons to making this election?

There are a few, however the biggest con is your individual income tax brackets. Tax brackets change based on your overall income every year. You would have to run the numbers to determine what would make the most sense – do you make the election or just wait and file it all together? Overall, this is super important to understand because it could mean you get more money back if you wait. A qualified tax professional should run this calculation for you.

How should everything be recorded on my books?

We could probably write an entire article just on this alone!

Some CPAs just understand tax compliance and don’t think about the bigger picture as it relates to your financial statements. You might have investors, banks and others reviewing your financials and tax returns on a regular basis. To make sure your business is on good footing I highly recommend that you take an active role in understanding how everything should be recorded on your books.

A business’s financials tell a story. Far too many business owners don’t look at them like that. When financial statements are provided to others and you aren’t available to explain them, they need to be able to effectively tell your story. Having a good team around you helps make sure your financials accurately tells your story so that anyone reviewing them can see there was a hurricane, you had some costs related to it, but you’re doing fine and figuring out what’s next. Paint a good picture of your business!

Here’s what to do in the following situations:

- Business interruption insurance money received: Record this to a new account called “Business interruption insurance income”. Group the account with your “Other Income & Expense” section.

- Inventory destroyed: Record any inventory losses to a new account called “Inventory Loss”. If you received insurance proceeds for the inventory, record it to the same account. Group the accounts in the “Other Income & Expense” section.

- Equipment destroyed: Usually equipment written off is recorded to an account called “Loss on disposal of equipment”. This would be applicable in this situation as well. If insurance proceeds are received for the destroyed equipment, record it the same account.

- Real estate partially or completely destroyed: A write down to your real estate and other property because of a decline in value due to the hurricane should be recorded to an account called “Hurricane Property Loss”. If insurance proceeds are received for the damaged or destroyed property, record it the same account.

- Other costs: Any other cost you have related to the hurricane should be recorded to a separate account such as “Hurricane related expenses.” This could include:

- Costs to protect your operations

- Costs to clean up after a hurricane

- Other costs that can be directly related to the hurricane

The purpose is to show that these aren’t normal operating costs. They’re anomies and shouldn’t be used in determining how well your business is doing year over year.

Do I get more time to file & pay my taxes?

After a hurricane, the last thing you want to worry about are your taxes. The IRS and most states will push back filing requirements and any related penalties (interest is always charged).

FEMA disaster declaration

With the IRS, and most states, FEMA must declare a federal disaster area for where you operate your business. FEMA keeps a list of all current and historical declared disasters along with information on various types of Federal support as well. If no federal disaster area is declared, you can’t use these benefits. Oh, and an interesting benefit, if your tax preparer is located in a federal disaster area, you get to follow these rules (even if your business is not located in a federal disaster area).

Internal Revenue Service (IRS)

The IRS' tax relief in disaster situations website provides up-to-date information to understand if the deadline to file your returns has been extended.

The IRS will also provide some relief to federally declared disaster areas. The IRS will typically:

- Push back filing deadlines by several months.

- Push back certain payment deadlines, such as quarterly estimated taxes.

- Provide penalty relief for certain late filing and payment deadlines.

While the IRS provides a little more time to make your payments and file returns, interest is never relieved. If you can, we recommend you make a payment of what you owe or think you will owe in taxes sooner rather than later. You’ll also want to get your returns filed by new deadline set by the IRS. If you don’t, you won’t be able to get out of the penalties and they can get fairly high very quickly.

Florida Sales Tax

Depending on the impact of the storm, the Florida Department of Revenue will typically push back any sales tax filing requirements and payment deadlines as well. The Florida Department of Revenue maintains an emergency information page that provides information on emergency orders and other important information such as adjusted due dates, adjusted payment dates and where you can go for support.

What if I can’t file my tax return because I haven’t received my K1?

If the LLC or entity you’ve invested in was located within a disaster area, the disaster rules are still applicable to you. Even though you aren’t in the disaster area, you’re covered by the disaster declaration. We always recommend paying an estimated tax payment anyway to prevent additional interest. Once the K1 comes in you can file your return and place a special code on the top of it indicating you are covered by the disaster declaration.

What if I need to move my business and/or myself because of the disaster?

First, I’m so sorry! Second, make sure to file a Form 8822 with the IRS letting them know your updated address. This is SUPER important so that you get your mail. It might make sense to get a PO Box at the post office for your business during this difficult time so that you always know where everything is going. During a disaster, the IRS will provide lots of information through the Tax relief in disaster situations section on their website.

The Bottom Line

Going through a hurricane isn’t fun. But hopefully with some of this knowledge, it makes it less stressful because now you know how hurricanes can impact your taxes. As long as you keep good records and work with a professional, you should be able to maximize your deductions and effectively manage your books through the chaos.

If you have experienced a casualty loss and need assistance, our team of experts at DiMercurio Advisors are more than happy to help you navigate these complex rules.