Keep your chart of accounts simple with these best practices.

Without a chart of accounts, it would be impossible to do your books. A chart of accounts is the list of all relevant accounts associated with running your business, which helps you categorize your transactions.

Your chart of accounts is an essential tool to help keep your books clean – as long as it’s simple, organized and easy to understand.

Every business’ chart of accounts will look slightly different. But regardless of size or industry, every business should follow these best practices.

What is a chart of accounts?

A chart of accounts is like a map that shows where your business is moving money, assets, debt or equity. It’s the complete list of all the accounts you’ll use when recording transactions in your books.

You need to create a chart of accounts before you can start bookkeeping. The categories you create should be used as a reference point when categorizing expenses – although most accounting software have default ones.

A chart of accounts is bound to look different for every business based on size and industry. Regardless of those factors, yours should be relevant to understanding and operating your business.

What types of accounts should I have?

There are five categories that every account in your chart of accounts should fall under.

- Assets: Accounts your business owns that provide value. Some examples include cash, property, land, equipment and trademarks.

- Liabilities: Accounts where you owe debt. Some examples include loans, salaries, mortgage and taxes.

- Equity: Accounts that are related to ownership. Some examples include retained earnings and current year earnings.

- Revenue: Accounts that earn you money. Some examples include sales, rent and interest.

- Expenses: Accounts that cost you money. Some examples include meals, supplies and advertising.

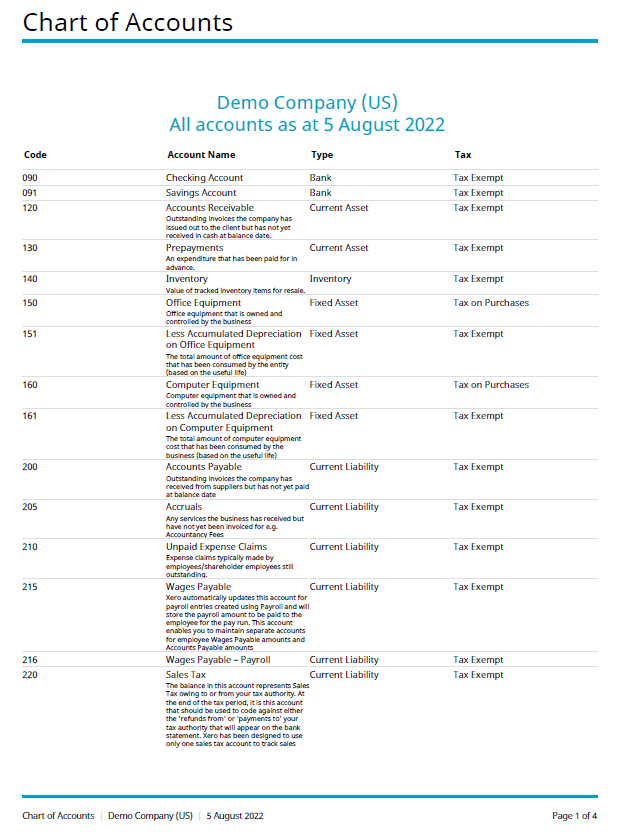

Within those categories, there should be more specific accounts on your chart of accounts. Here’s a part of what a simple chart of accounts should look like:

How many accounts should I have?

An average small business owner’s chart of accounts can range from 50 to 100 accounts. Depending on your business and industry, you may have more or less.

The quantity of your accounts can have a big impact on your books – and potentially your taxes and other areas of your business’ finances.

If your chart of accounts has too many accounts, you can create more work for yourself. Your transactions will take longer to categorize and reconcile, and you could risk missing out on tax deductions.

A common area small business owners tend to overcomplicate their chart of accounts is travel. Instead of having one account for travel expenses, they might make separate accounts for fuel, tolls, flights, parking and more. Unless it’s absolutely necessary, creating more accounts just opens up the opportunity for more mistakes.

On the other hand, it can also be harmful to have too few accounts. If you’re placing a loan principal and interest in the same account, for example, that would cause issues on your tax return – since interest is tax-deductible, and principal is not.

Hiring a bookkeeper or accountant to guide you through an effective chart of accounts can make it accurate and easy to use.

Best practices for creating a chart of accounts

Your chart of accounts should be a simple, but important reference point to use for your business. Here are some things to keep in mind when creating and maintaining your chart of accounts:

Create your chart of accounts before you start bookkeeping

You should have a solid chart of accounts before you start doing your own bookkeeping. If you haven’t started making transactions, ask yourself these questions to get an idea of what accounts you need to create:

- Do I need multiple inventory accounts?

- Are there specific expenses I need to monitor?

- Am I going to need one or multiple sales accounts?

You can also talk to your CPA, attorney or accountant to find out what accounts you may need.

Create or delete accounts deliberately

Don’t be flippant about editing your chart of accounts. Every account you create, delete or consolidate can impact your books – or even your taxes. Your chart of accounts is an organizational tool, so make sure any changes you make are necessary and make your bookkeeping better.

Review your chart of accounts regularly

Reviewing your chart of accounts on a quarterly or annual basis can help you find ways to improve it. You still shouldn’t be flippant about changing it, but you should make sure all your accounts are still relevant.

Standardize your labeling system

Any account on your chart of accounts should have a number attached to it. This helps you keep your accounts organized – and can signify the type of account. A standard numbering system could look like this:

- Assets: 100-199

- Liabilities: 200-299

- Equity: 300-399

- Revenue: 400-499

- Expenses: 500-599

The bottom line

Your chart of accounts lists every account associated with your business’ assets, liabilities, equity, revenue and expenses.

It’s a simple thing to put together, but there are still some best practices when it comes to creating one. You don’t want to break every little expense into its own account, but you also don’t want to create so few accounts that you’re grouping unrelated transactions together.

If you need help with creating your chart of accounts – or your bookkeeping altogether – schedule a free call with a DiMercurio Advisors team member. Let an expert handle your books so you could spend more time focusing on the parts of your business you actually love.